Colorado Supreme Court rejects business group’s challenge to secretary of state on fees

The Colorado Supreme Court on Monday rejected a claim from the Colorado chapter of the National Federation of Independent Business that business fees collected by the Secretary of State’s Office are actually taxes and hence should be approved by voters under the state Taxpayer’s Bill of Rights.

The Supreme Court’s decision comes just two months after a federal appeals court granted a request for an appeal by a group of former elected officials who seek to have TABOR declared unconstitutional.

In its unanimous ruling Monday, the court said the 2014 lawsuit “provides us another opportunity to examine the implications” of TABOR.

“At issue now is how Colorado’s Department of State charges for some of its services — for example, licensing businesses — to then fund its general operations, which include overseeing elections,” which NFIB, a small-business advocacy group, argued was unconstitutional under TABOR.

The question the court examined was whether the Department of State’s occasional decisions to adjust its business fees — which has been in place since 1983, well before TABOR was approved by voters — violates TABOR’s requirement that any tax increases first win voters’ OK.

NFIB argued that the fees are really a tax, because some of those fees cover the general operations of the Department of State, such as elections, in addition to financing the department’s business division.

The NFIB also argued that because the fees are really a tax, any increases would have to be submitted to voters for approval.

“There was no evidence to establish that any post-TABOR adjustments (adjustments to the fee after TABOR passed in 1992) resulted in a new tax, tax rate increase, or tax policy change directly causing a net revenue gain,” the court wrote in its opinion. “The Secretary [of State] has the discretion to set, increase, decrease, or temporarily suspend the Department’s charges without legislative oversight.”

The court noted that a lower court initially granted summary judgment to the Department of State, examining only whether the funding scheme was unconstitutional.

“In doing so, it declined to determine whether the charges were taxes because it concluded the funding statute wasn’t subject to TABOR at all,” the Supreme Court ruling stated.

The appellate court disagreed in its reversal of the lower-court decision.The appellate court declined to determine whether TABOR applied to increases in business and licensing charges, and so the matter was off to the state’s high court.

The Supreme Court reminded the parties that TABOR doesn’t apply to all taxing, revenue, and spending actions. Because it is prospective, it only applies to any “new taxes,” “tax rate increases,” or “tax policy changes” that directly causing a net revenue gain.

And those terms — new taxes, tax rate increases or tax policy changes — aren’t defined in TABOR, so the court has, over the years, tried to provide guidance. In one case, the Supreme Court opinion pointed out that it “suggested that there may not be one all-encompassing definition of either ‘tax’ or ‘tax rate.'” And in a recent ruling involving the TABOR Foundation, the court pointed out that “new tax” and “tax policy change” implied something significant, not just a minimal change.

In its arguments, NFIB pointed out that in 1996, the Secretary of State began using revenue from the business fees to pay for elections. That constituted a new tax or new tax policy, NFIB argued. But the Supreme Court said there was no evidence submitted that showed an increase in fees to pay for those specific functions.

NFIB also showed changes in the fees over the years, but the court said that those adjustments, which it called necessary to cover a fourfold increase in service requests, didn’t “create a new tax, tax rate increase, or a tax policy change directly causing a net revenue gain,” so “then the adjustments don’t trigger TABOR.”

“We are of course disappointed with the court’s decision, however, Colorado businesses should be thoroughly disappointed with the court’s lackadaisical attitude in examining the fee-versus-tax issue,” said Tony Gagliardi, Colorado state director for NFIB.

Karen Harned, executive director of the NFIB Small Business Legal Center, said the decision “leaves unresolved whether and to what extent the Secretary [of State] may continue increasing fees on the small business community; however, our lawsuit has put the secretary on notice that we will scrutinize increased charges going forward.”

Aurora seats new progressive council

Kyla Pearce

kyla.pearce@gazette.com

Updated 6 hours ago

Aurora’s four new councilmembers and an incumbent were sworn in Monday night, marking the beginning of a progressive-majority council rule in the city that has been led by conservatives for years. “This is what democracy looks like,” new at-large member...

Dean alleges firing over opposition to book ban in Elizabeth School District

Deborah Grigsby

deborah.smith@denvergazette.com

Updated 9 hours ago

A former Elizabeth Middle School dean of students has filed a lawsuit in federal court alleging she was terminated because of her opposition to the district’s book ban policy and her advocacy against “racism” in the school. On Nov. 30,...

Heading into holidays, shoplifting on the rise in Colorado, study says

Mark Samuelson Special to The Denver Gazette

mark.samuelson@denvergazette.com

Updated 9 hours ago

Shoplifting and other forms of retail crime are seeing a sharp rise as Colorado heads into the holidays, according to a study. After falling from a recent-record 24,975 thefts reported in 2015 to around 18,000 in 2021, Colorado Bureau of...

Funeral for Sen. Faith Winter will be held Friday at the Colorado Capitol

Marianne Goodland

marianne.goodland@coloradopolitics.com

Updated 9 hours ago

Colorado Sen. Faith Winter will be remembered on Dec. 5 at 2 p.m. in a funeral service on the state Capitol’s west steps. A celebration of life reception will follow. Winter died on Wednesday, Nov. 26, in a three-vehicle accident...

10th Circuit rules Greeley officer unconstitutionally detained man standing outside home

Michael Karlik

michael.karlik@coloradopolitics.com

Updated 10 hours ago

The Denver-based federal appeals court concluded last week that a Greeley police officer lacked reasonable suspicion to detain a man who was standing outside the door of a residence and not engaging in any indicators of criminal activity. A three-judge...

Copper Creek yearling wolf blamed for livestock death in Gunnison County

Marianne Goodland

marianne.goodland@coloradopolitics.com

Updated 10 hours ago

A heifer found dead in eastern Gunnison County on Nov. 22 was killed by one of the yearlings from the Copper Creek wolf pack, according to a rancher, who did not want to be identified. It’s the fourth livestock death...

‘Utterly no precedent’: Federal judge expresses concerns about Jeffco’s early appeal in jail death case

Michael Karlik

michael.karlik@coloradopolitics.com

Updated 9 hours ago

A federal judge shared his concerns on Monday about Jefferson County’s appeal of a routine procedural order in a constitutional rights case, which the plaintiffs argued could spawn appeal-related delays in countless lawsuits against the government. During a hearing, U.S....

Justice Hart’s absence continues, state Supreme Court hears oral arguments | COURT CRAWL

Michael Karlik

michael.karlik@coloradopolitics.com

Updated 13 hours ago

Welcome to Court Crawl, Colorado Politics’ roundup of news from the third branch of government. One member of the Colorado Supreme Court remains on an unusual leave of absence, plus the court heard oral arguments in eight more cases last...

Denver Art Museum gala honors treasured benefactors Kent and Vicki Logan | NONPROFIT REGISTER

Joanne Davidson Special to Colorado Politics

joanne-davidson-special-to-colorado-politics@coloradopolitics.com

Updated 13 hours ago

DENVER ART MUSEUM Denver News: Kent and Vicki Logan, who 25 years ago made the largest gift in the history of the Denver Art Museum’s modern and contemporary art department, were the honorees when the DAM hosted the 43rd edition of its...

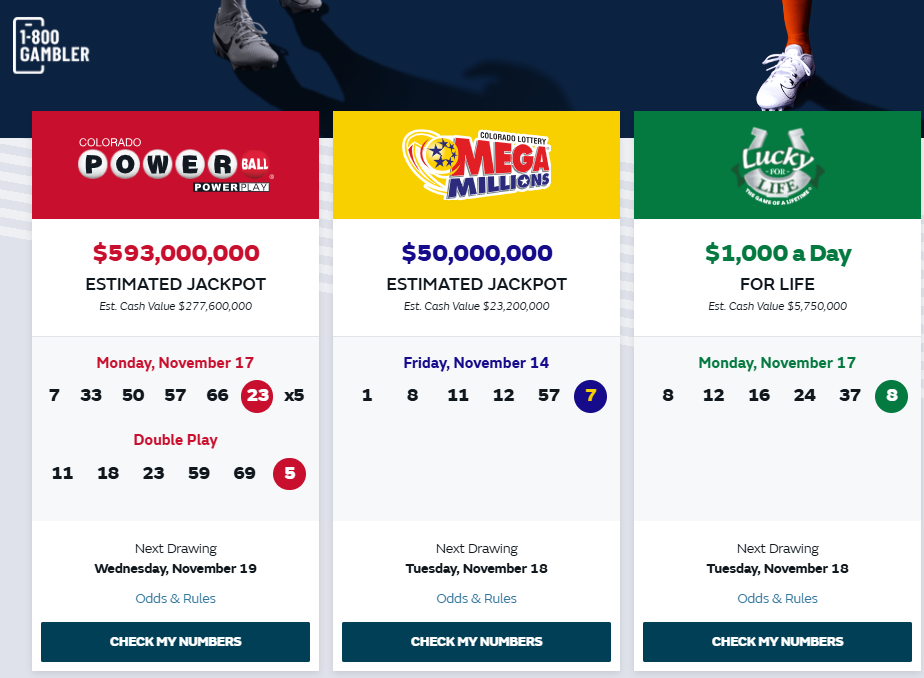

The Colorado Lottery’s mega-bad idea | Sondermann

Eric Sonderemann

eric-sonderemann@coloradopolitics.com

Updated 17 hours ago

There are plenty of lousy, miserable, misguided whims out there. Then, every so often, you come across a notion so wrong-headed that it qualifies as phenomenally bad. Or, in words the marketing whizzes at the Colorado Lottery might understand, let’s...

PREV

PREVIOUS

Colorado Attorney General Phil Weiser weighs in on proposed 'Jaime's Law'

Colorado Attorney General Phil Weiser on Monday signed onto a letter to Congress from 21 attorneys general who want to see action on Jaime’s Law. The proposed law, sponsored by Democratic Rep. Debbie Wasserman Schultz of Florida, is named for Jaime Guttenberg, a 14-year-old student who died in the Feb. 14, 2018, shooting at Marjory […]

Denver City Council to weigh 21+ tobacco law, amendments to historic landmark rules Monday night

The Denver City Council is expected to vote Monday night on whether to advance a proposed law that would raise the minimum age to buy tobacco products from 18 to 21. The bill, which the council is considering at the request of the Denver Department of Public Health & Environment, would cover all products containing […]