Colorado Supreme Court rejects ‘perverse’ incentive for foreclosures

The Colorado Supreme Court on Monday rejected a lower court’s interpretation of the law that could have encouraged mortgage lenders to foreclose more quickly on homeowners exiting bankruptcy, calling the effects of such a ruling “perverse.”

The issue before the justices was what impact a homeowner’s discharge from bankruptcy has on the timeline for banks to foreclose, assuming there are no more payments on the mortgage. Under Colorado law, a lender has six years to initiate a foreclosure after a payment becomes due.

But when someone exits bankruptcy and no longer has the obligation to make mortgage payments, does the entire mortgage become due then?

No, said the Supreme Court.

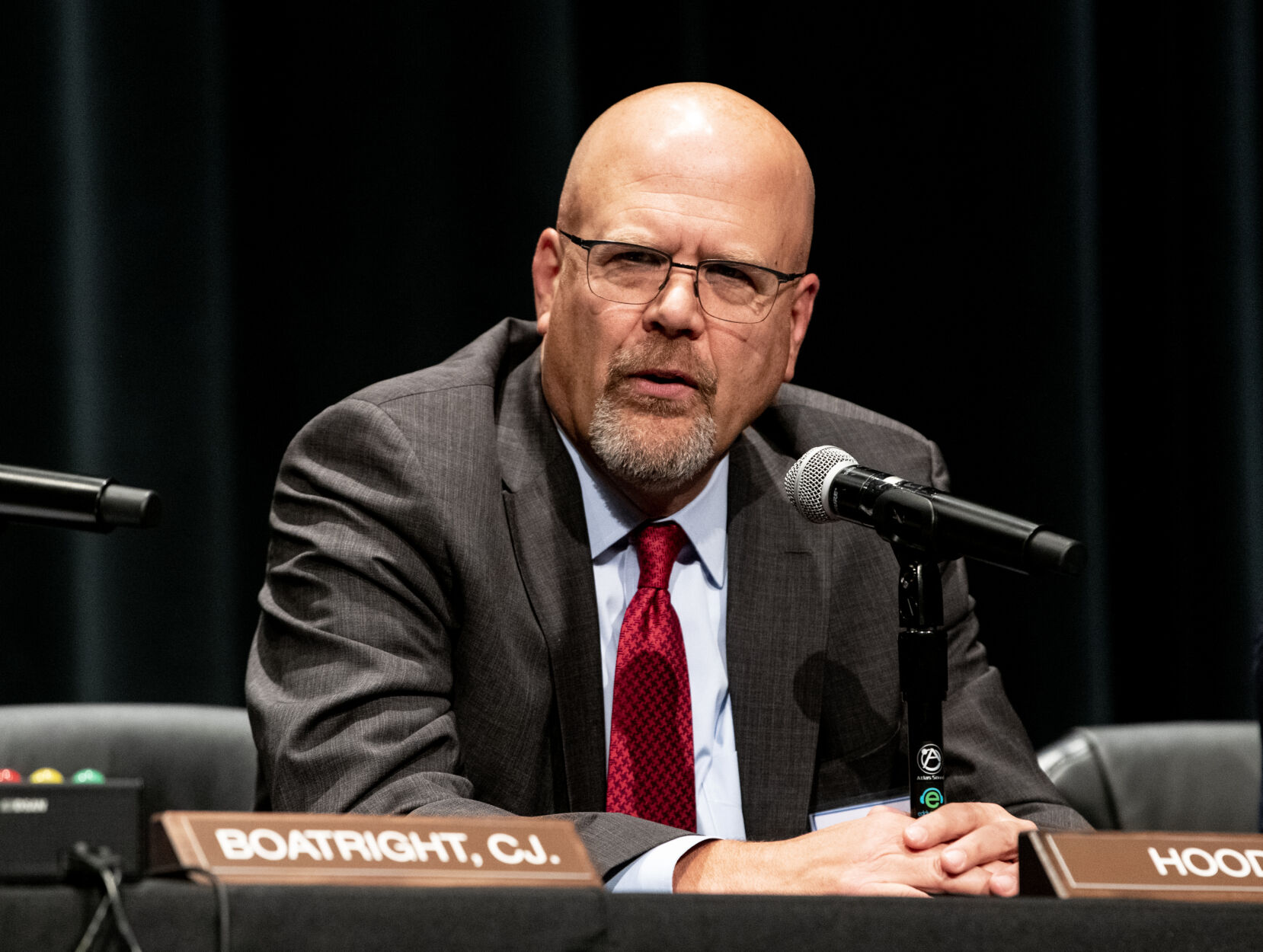

“If a security agreement mandates regular monthly payments, as it does here, the debt becomes due when each installment is missed,” wrote Justice William W. Hood III in the court’s April 24 opinion. Therefore, the six-year statute of limitations will apply through the end of the mortgage’s lifetime – typically 30 years – during which a homeowner may choose to continue making payments even after bankruptcy.

In the underlying lawsuit, Jerome D. Silvernagel and Dan Wu sought a court’s declaration that they owned their Highlands Ranch house in the face of efforts to foreclose on them. Silvernagel took out a second mortgage in 2006, but stopped making payments after he exited bankruptcy in 2012. The lender, U.S. Bank National Association, allegedly did not demand payment until more than six years later, when it attempted to foreclose.

Both sets of parties argued their reading of the law would benefit homeowners. Silvernagel and Wu believed it was unreasonable for banks to lie in wait for years, hoping a home’s value will increase, before suddenly demanding payment or attempting to foreclose. U.S. Bank, on the other hand, pointed out that requiring lenders to foreclose for nonpayment within six years of a bankruptcy – or else forfeit the ability to ever recover the house – would only encourage more foreclosures.

The Court of Appeals originally sided with Silvernagel and Wu, concluding the men were essentially entitled to a “free house” if U.S. Bank had, in fact, waited more than six years after bankruptcy to attempt to foreclose. In doing so, the court relied on a case out of Washington, whose law is similar to Colorado’s.

In that case, then-U.S. District Court Judge Ronald B. Leighton had interpreted the precedent on bankruptcy discharges to mean a mortgage becomes due when the borrower no longer has liability to make payments – that is, when they exit bankruptcy. Therefore, the six-year clock started at that moment.

Other courts, including in Colorado, parroted Leighton’s reading of the law until last year, when the Washington Court of Appeals stepped in to say Leighton had misread its prior rulings. There was no rule that entire mortgages become due upon a bankruptcy discharge.

While the Washington Supreme Court is currently reviewing the conclusion of its appellate court, Colorado’s highest court distanced itself from what it called the “disputed case law from the state of Washington.”

Hood, in the court’s opinion, cited a 2011 study co-authored by an economist at the Federal Reserve Bank of Philadelphia, finding bankruptcy allows borrowers to use more of their income for mortgage payments by discharging certain debts. Consequently, bankruptcy provides homeowners “breathing room” to repay their mortgages and remain in their houses.

“This feature is a significant benefit for borrowers: bankruptcy does not automatically enable a lender to foreclose on a property,” Hood wrote. “If upheld, the (Court of Appeals’) rule would have the perverse result of making it more difficult for individuals in bankruptcy proceedings to keep their homes.”

That conclusion echoed observations the justices made during oral arguments last month, in which the court seemed skeptical of endorsing Silvernagel and Wu’s request for speedy post-bankruptcy foreclosures on homeowners.

“What it would force the bank to do is foreclose when they would lose money and it would force your clients out of the house,” Justice Richard L. Gabriel told their attorney. “It seems everybody loses.”

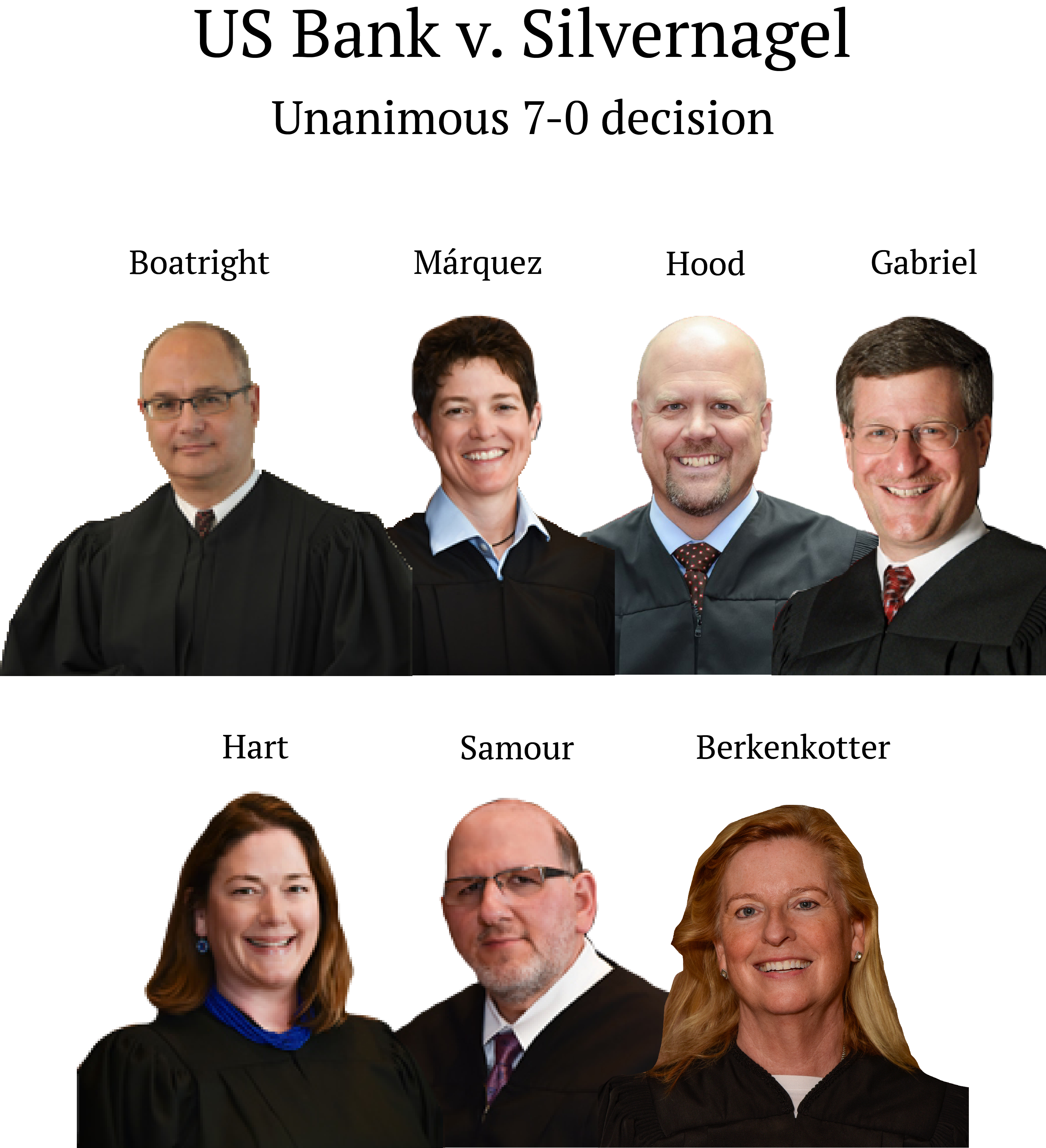

The case is U.S. Bank National Association v. Silvernagel et al.

Divided 10th Circuit lets Colorado enforce interest rate cap on out-of-state banks

Michael Karlik

michael.karlik@coloradopolitics.com

Updated 1 hour ago

The Denver-based federal appeals court ruled on Monday that Colorado may use a decades-old provision of federal law to require out-of-state banks to abide by Colorado’s maximum interest rates when they lend to in-state residents. A three-judge panel of the...

Colorado Supreme Court suspends rules for ‘Indian child’ welfare cases

Michael Karlik

michael.karlik@coloradopolitics.com

Updated 4 hours ago

The Colorado Supreme Court suspended its rules last week that govern how judges handle custody cases when an “Indian child” is involved. The court’s move came after the legislature enacted extensive changes this year, partially in response to Supreme Court...

Appeals judge raises questions about review of custody decisions

Michael Karlik

michael.karlik@coloradopolitics.com

Updated 8 hours ago

A member of Colorado’s second-highest court suggested last week that appellate judges should have more leeway to decide whether trial judges correctly terminate or decline to terminate parents’ legal rights over their children. At the same time, the three-judge Court...

County court judge suspended pending investigation, Supreme Court committee advances eviction rule | COURT CRAWL

Michael Karlik

michael.karlik@coloradopolitics.com

Updated 1 day ago

Welcome to Court Crawl, Colorado Politics’ roundup of news from the third branch of government. A San Miguel County judge is on suspension pending a misconduct investigation, plus a Colorado Supreme Court committee advanced a rule change designed to benefit...

Colorado justices: El Paso County judge erred by removing prosecutor for comments about stabbing public defenders

Michael Karlik

michael.karlik@coloradopolitics.com

Updated 23 hours ago

The Colorado Supreme Court, by a 5-1 vote, concluded on Monday that an El Paso County judge mistakenly removed a prosecutor from a murder case after he was overheard saying he hoped the defendant would stab public defenders if he...

Two charged with murder of woman in Westminster parking lot

Sage Kelley

sage.kelley@denvergazette.com

Updated 1 day ago

Two men face murder charges after a fatal shooting in Westminster last month. The 17th Judicial District Attorney’s Office said it officially filed murder charges against 19-year-old Daniel Romero and 24-year-old Michael Fernandez, Jr. on Monday morning. The charges stem...

A brief overview of The GEO Group v. Menocal, the class action out of Colorado about immigration detention

Michael Karlik

michael.karlik@coloradopolitics.com

Updated 1 day ago

On Monday, the U.S. Supreme Court heard oral arguments in the case of The GEO Group v. Menocal, which originated in Colorado. The arguments revolved around when appeals courts may review claims by federal contractors that they are immune from...

Colorado Supreme Court committee advances tenant-friendly rule change

Michael Karlik

michael.karlik@coloradopolitics.com

Updated 1 day ago

The Colorado Supreme Court’s Civil Rules Committee advanced a proposal on Friday that would make it easier for tenants facing eviction to respond to and learn about their landlord’s initial court filing. Several members of the committee were torn about...

Appeals court reverses Fremont County judge’s sanction on DA’s office over evidence misunderstanding

Michael Karlik

michael.karlik@coloradopolitics.com

Updated 4 days ago

Colorado’s second-highest court ruled on Thursday that a Fremont County judge was wrong to reduce the severity of a criminal charge because she believed the district attorney’s office failed to turn over police reports that, in reality, did not exist....

Judicial discipline changes moving at a slow pace

David Migoya

david.migoya@gazette.com

Updated 1 hour ago

Colorado’s judicial system is barely closer to fixing what some have called a broken process of disciplining judges a year after voters approved a new method of dealing with the issue and eight months after revelations the state fosters a...

PREV

PREVIOUS

Bill offering free bleed control kits for schools passes Colorado legislature

Colorado lawmakers approved a bill to offer schools free bleed control kits on Monday, advancing the proposal to Gov. Jared Polis for final consideration. If signed into law, House Bill 1213 would provide free bleed control kits and training materials to K-12 schools that request them. Bleed control kits are first aid kits designed to control serious […]

Colorado Supreme Court clarifies juvenile defendants can immediately appeal competency findings

When a magistrate decides whether a juvenile defendant is competent to stand trial, that determination is appealable to a judge right away, Colorado’s Supreme Court ruled on Monday. Addressing a question it had never before answered, the court acknowledged there would be significant consequences if a child were to proceed to trial despite actually being […]