Pinnacol releases ‘market-based’ estimate of paid family and medical leave program

A new estimate of the costs of a paid family and medical leave program from Pinnacol Assurance shows a market-based approach might result in lower costs and premiums for a low-benefit program, but much higher costs and premiums for a “Cadillac”-type plan.

Pinnacol, the state’s largest provider of worker compensation insurance, used much of the same data that made up the actuarial analysis provided to a state task force that released its final report earlier this month.

The proposed leave program that has been the darling of Democrats for several years provides partial wage replacement to eligible workers who need to take time off, and would primarily benefit low-wage workers. Those eligible for the program could take leave for bonding after childbirth, caring for family members, military service-related leave, personal disability, domestic violence, sexual assault and/or stalking, and organ donation.

A low-benefit plan would provide up to six weeks of paid leave or 12 weeks over a year; a high-benefit, or Cadillac-type plan, would cover up to 14 weeks of paid leave or 28 weeks over a year’s time.

Senate Bill 19-188, which, as introduced, would have put the plan on the road to implementation, ran into trouble in the 2019 session and was turned into a study.

Opponents pointed out that these types of programs are already offered by some employers, including local governments, and that forcing a second program into the market could mean businesses might eliminate more generous programs.

Over the summer and fall, a task force has reviewed at options and contracted with AMI Risk Consultants of Miami to conduct an actuarial study of the short-term and long-term solvency of a paid family and medical leave program.

Pinnacol, in a presentation to the task force in October, pointed out experience in other states, including New York. That included slow claims processing, accuracy problems and rate increases. New York’s plan experienced a 70% increase in premium rates in the state-run program’s first year because of higher-than-expected utilization rates and mandated automatic benefit increases. At that time, Pinnacol recommended a plan to be run by private carriers.

“We believe a market-based approach” on paid family and medical leave offers advantages, the Pinnacol report, released Tuesday, said. “This desire to look for a market-based alternative came from the business community that believed a state-run plan wasn’t viable,” according to Edie Sonn of Pinnacol.

Pinnacol Chief Financial Officer Kathy Kranz said their actuarial analysis was based on industry and size of company, rather than a statewide analysis as was done by AMI.

“The report tells us that there are demographics by industry that drive differences in pricing,” Kranz said Thursday.

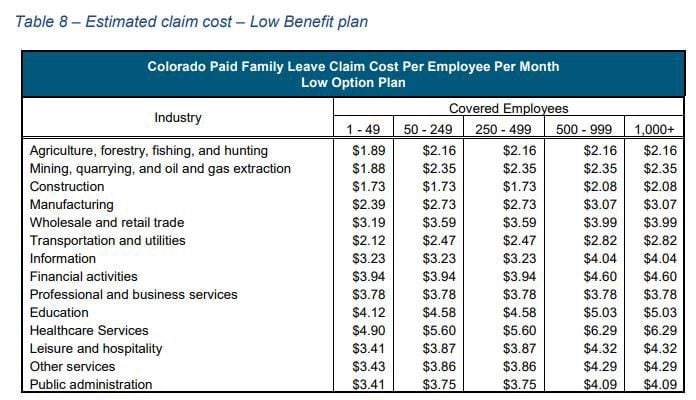

Family leave claims costs by industry. Costs are substantially higher for medical leave, according to the Pinnacol report. Courtesy Pinnacol Assurance.

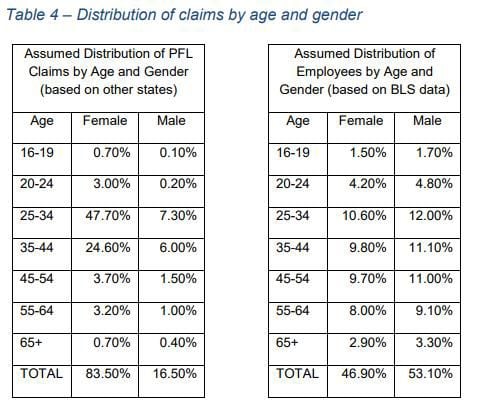

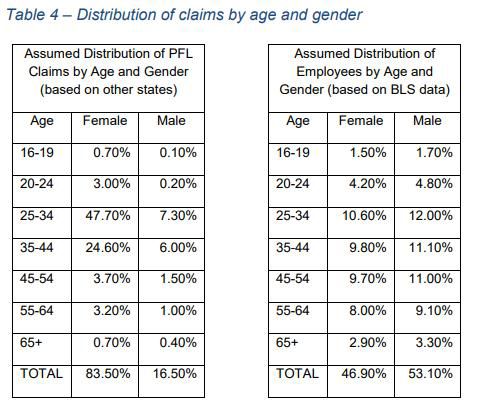

Family leave claims usage by age and gender that shows claims usage is highest for employees in the maternity leave age demographic. Usage is substantially higher for older employees for medical leave. Courtesy Pinnacol Assurance.

Among the biggest differences between the AMI report and Pinnacol’s: a market-based plan could be ready to offer benefits as soon as 2022; the leave program analyzed by AMI estimated a start date for benefits of 2024, since the plan would require up to two years of premium payments before its launch.

Another major difference is in who actually would pay into the plans. Both AMI and Pinnacol assumed a salary cap of $90,000 for the low-benefit plan. It’s somewhat similar to how Social Security and Medicare work: Once your salary has gone above a certain dollar amount — for Social Security, the cap in 2019 is around $133,000 per year — you no longer pay into the system although you are still eligible for benefits.

Pinnacol’s assumption, using more precise data, according to Kranz, is that there would be more salaries that would come in above the cap and at that point, those employees would stop paying premiums to the plan, although they would still be eligible for plan benefits. That made a 10% difference in claims projections, Kranz explained.

AMI did not look at start-up costs that would be borne by taxpayers, although the fiscal note on SB 188 estimated those start-up costs at around $75 million. Pinnacol’s report said a market-based plan would save $24 million off that tab. That’s due to a difference in how those plans are funded. Kranz said the state would collect the tax for a year but not provide benefits; that’s how they fund the start-up costs. The start-up costs estimated by Pinnacol builds up the risk fund while at the same time providing benefits as soon as the plan is paid for by a business.

And then there’s the cost and time required to set up the state bureaucracy needed to run the plan. Pinnacol said a state-run plan could require up to 300 additional employees for the department of Labor and Employment, nearly 100 more than estimated by SB 188’s fiscal note.

There’s other benefits in a market-based plan, the Pinnacol report said. It assumes that some large employers will choose to self-insure, an option not available under the AMI analysis.

Year one premiums for a low-benefit market-based plan, to be paid by both employers and employees, would cost $1.076 billion to $1.266 billion. AMI’s final report estimated those costs at $1.168 billion.

Average premiums for the low-benefit plan under the market-based approach would average .69% to .81% of payroll, compared to .71% for the low-benefit plan analyzed by AMI.

For the high-benefit plan, however, the market-based approach came in considerably higher: $2.69 billion to $3.17 billion, versus $2.29 billion for the high-benefit plan analyzed by AMI.

Premiums would be higher too; for the high-benefit market-based plan, at 1.56% to 1.85% of payroll, compared to 1.18% of payroll as estimated by AMI.

Kranz explained that the ranges offered in the Pinnacol estimate, rather than the precise points in the AMI analysis, are because claim costs are so uncertain and because there is so little data on these kinds of programs. Pinnacol’s actuarial assumptions also estimated slightly higher claim costs than AMI’s estimate for the low-benefit plan and much higher claims costs for the high-benefit paln, also due to the uncertainty around these kinds of plans, she said.

“The actuarial assumptions reflect a wide range of possible outcomes.”

Colorado Politics Must-Reads:

Heat, wind and drought conditions spark wildfires across US West | OUT WEST ROUNDUP

Ernest Luning

ernest.luning@coloradopolitics.com

Updated 3 hours ago

Heat, drought spark wildfires Extreme heat and dry, windy conditions fueled several wildfires in the West on June 21, including an uncontained blaze in Utah that forced the evacuation of a small town southwest of Salt Lake City. The Iron...

Crank challenger Jessica Killin signs on to new centrist Democratic group’s ‘Promise to America’

Ernest Luning

ernest.luning@coloradopolitics.com

Updated 12 minutes ago

Jessica Killin, one of the Democrats running in Tuesday’s primary for the chance to challenge U.S. Rep. Jeff Crank in Colorado’s 5th Congressional District, joined with more than a dozen incumbent Democratic lawmakers and candidates this week signing on to...

Colorado Politics Calendar June 29-July 5

Rachael Wright, Special to Colorado Politics

rachael.wright@coloradopolitics.com

Updated 4 days ago

CoPo’s weekly political calendar will help you find political and public-policy events throughout Colorado. It includes candidate and issue campaign events, public policy meetings, court hearings, state and local party conventions, assemblies, debates, rallies, parades, speaking engagements, traveling dignitary appearances,...

Gov. Lamm’s GOP challenger gives insights into his campaign | A LOOK BACK

Rachael Wright, Special to Colorado Politics

rachael.wright@coloradopolitics.com

Updated 4 days ago

Forty-five years ago this week: “I see Gov. (Richard) Lamm is fairly popular in general,” said gubernatorial candidate and state Sen. Bill Hughes, R-Colorado Springs. “ … And he’ll be hard to beat.” Hughes was on a whirlwind campaign trail...

Giving credit to Polis where credit is due | SONDERMANN

Eric Sondermann

eric-sondermann@coloradopolitics.com

Updated 4 days ago

It is an understatement to suggest that Gov. Jared Polis has had a tough couple of months. The bloom was already off the rose and Coloradans were paying far more attention to the choice of his replacement than they were...

Bennet, Hickenlooper to vote against Trump’s 10th Circuit nominee from Colorado

Michael Karlik

michael.karlik@coloradopolitics.com

Updated 1 day ago

Colorado’s two Democratic senators will not vote to confirm President Donald Trump’s nominee to a vacancy on the Denver-based federal appeals court. Trump has selected U.S. District Court Chief Judge Daniel D. Domenico, who he appointed as a federal trial...

Who’s spending in Colorado to get your vote?

Marianne Goodland

marianne.goodland@coloradopolitics.com

Updated 1 day ago

Groups that raise unlimited amounts of money have spent about $20 million in May and June to try and influence Colorado voters’ choices in the upcoming June 30 primaries. By law, these groups cannot coordinate with the candidates they support....

U.S. government declines to oppose multiple challenges to immigration detention in Colorado

Michael Karlik

michael.karlik@coloradopolitics.com

Updated 2 days ago

Multiple federal judges in Colorado granted petitions from people challenging the lawfulness of their immigration detention this week after the government took the unusual step of declining to submit arguments in opposition. Colorado’s federal trial court is facing a flood of...

Tina Peters tells supporters to ‘stand up and fight back’ at Castle Rock event

Marissa Ventrelli

marissa.ventrelli@coloradopolitics.com

Updated 2 days ago

Tina Peters, the former Mesa County clerk recently released from prison, warned supporters that what happened to her could happen to them, too, if they did not “stand up and fight back” at an event at the Douglas County Fairgrounds....

Iran strikes cargo ship in Strait of Hormuz, endangering Trump’s peace

Christian Datoc

christian-datoc@coloradopolitics.com

Updated 2 days ago

Iran attacked a cargo ship traveling through the Strait of Hormuz on Thursday, possibly upending President Donald Trump‘s diplomatic end to the war with Iran. A U.S. official confirmed to the Washington Examiner that the Islamic Revolutionary Guard Corps “struck...

PREV

PREVIOUS

Drought report shows tough days ahead for Southwestern Colorado

Thursday’s report from the United States Drought Monitor shows the month of December has not been kind to most of Colorado. Drought conditions statewide have jumped to 68% of the state, with potential impacts on dryland and winter farming and ski areas. But it’s better than a year ago, when 84% of the state was […]

LEGISLATIVE PREVIEW | Mental health advocates assess gains, see 'a long way to go'

After steering numerous pieces of landmark legislation into law in the 2019 session, Colorado’s mental health care advocates are looking to close gaps in coverage and address issues one lawmaker calls the missing pieces in the puzzle with a focused set of proposals set to be introduced in the General Assembly’s upcoming session. Bills in […]